Can innovations in logistics and financial services benefit actors throughout agricultural value chains?

Catalyzed by changes to global markets, urbanization, and other trends, agri-food value chains have been growing and changing rapidly in low- and middle-income countries (LMICs) over the past few decades. Perhaps more than ever, even in the world’s poorest countries, farmers can access high-value consumer markets both domestically and abroad. Benefiting from access to these high-value markets, however, often requires that crops meet specific quality, reliability, and volume standards. However, smaller agri-food value chain actors—farmers, aggregators, traders, processors or others—may not operate at a large enough scale to make traditional investments required to meet those standards, therefore hindering their ability to participate in new, more remunerative markets.

Recent innovations in both logistics and financial services—and sometimes both—could play a role in reducing transaction costs for participation in higher value markets by both smallholder farmers and SMEs moving food from farms to retail markets. Firms like Twiga Foods in Kenya, Ninjacart in India, Pinduoduo in China, and Tanihub in Indonesia have all created different types of digital marketplaces for agricultural products using technology to match agricultural products to different types of consumers or retail outlets. These digital hubs have the further advantages of improving traceability and therefore the assurance of food safety, particularly for perishable products; and they can also democratize price information, reducing arbitrage opportunities across markets.

Digital financial services may have similar benefits for smallholders and SMEs in LMICs. If farmers have access to credit or liquidity at specific times in the production cycle, they can increase both their product quality and overall profitability. SMEs in the midstream of value chains also have specific credit needs that may not be met by markets. As with logistics, digital technology lends itself well to increasing the availability of finance in agriculture. Credit applications among producers can be enhanced or even collateralized using digital financial services; mobile money can be used both as an efficient method of paying farmers and as a savings vehicle; and insurance products can use satellite data to improve risk models.

While technology can improve the availability of both logistics and digital financial services, it is not clear which value chains and markets might be able to effectively adopt them, and whether they will have positive incomes on smallholder and SME income if adopted. Therefore, as part of CGIAR’s Rethinking Food Markets Initiative, we are undertaking studies in Bangladesh, Nigeria, and Uganda to understand how different schemes that link smallholders and/or SMEs to modern logistics or digital financial services can potentially raise incomes among smallholders and SMEs participating in specific value chains.

One clear “necessary condition” relates to the difference in value placed on crops as they leave the farm and the value placed on products as they reach end markets. Larger differences between these prices reflect transportation costs, risks to owning products that could spoil, and rents accruing to value chain actors between the farmgate and wholesalers or processors. If a specific value chain actor both has market power locally and can act upon it, then it will capture higher rents from trade in the value chain. It is important to note that returns to agri-food value chain activities are based both on volume and the difference between revenues and costs. By increasing product quantity in the value chain, through improved credit, specific actors can make as much or more by increasing volume even if their rents on a per unit basis decline.

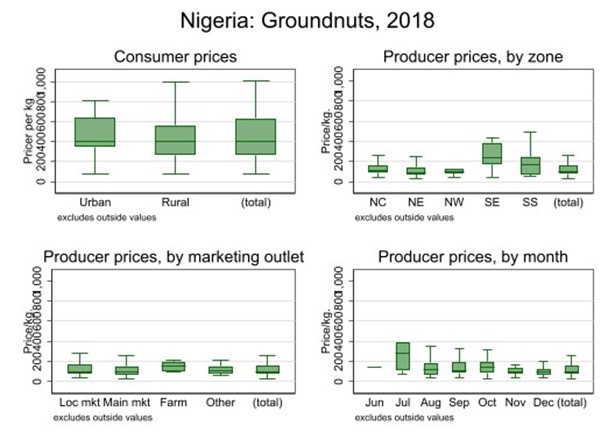

To illustrate, consider a snapshot of the groundnut market in Nigeria in the figure below. Consumer prices—whether in urban or rural areas—are around 400 Naira/kilogram in the 2019 GHS survey data, at the median (top left corner). Yet they sell at prices between 100 and 200 Naira in most local markets, with lower prices in the North and higher prices in the South. The data further exhibit seasonality—prices are higher in July than later in the year (bottom right). This difference can be explained by transport costs—the majority of the population, and therefore demand, is located in the South. That all said, the data illustrate a consistent gap between consumer and producer prices, implying that there is value being spread to other actors in the value chain of about 200 to 300 Naira/kilogram. Assuming that some of this gap could be narrowed through improved financial services or logistics, producers, consumers, and some value chain actors could all benefit. Moreover, higher prices paid to producers could in turn increase supply, and lower prices paid by consumers could increase demand as well.

Figure: Consumer and Producer Prices for Groundnuts in Nigeria over time, Nigeria General household Survey, 2018/9

In 2023, we plan to document more of these price differentials to understand where the most potential lies to help reduce transaction costs between producers and consumers. We are also beginning pilot projects designed to rigorously demonstrate how new technologies and ideas regarding logistics and finance can help increase smallholder and SME incomes.

Rethinking Food Markets Initiative thanks all funders for supporting this research through their contributions to the CGIAR Trust Fund, and in particular the Bill and Melinda Gates Foundation for designated funds received.